Retail strategy often breaks down whenever we try to go around accurate data. Clicks are random, surveys are incomplete, and intent doesn’t always translate into action. What does? Card and POS transactions. They reveal what people actually buy, where, how often, and for how much — insights that sit at the core of effective retail media solutions. Personalisation built on that truth tends to pay. McKinsey has put numbers to it for years: done well, personalisation lifts revenue by roughly 5–15% and materially improves marketing ROI.

What counts as transaction data?

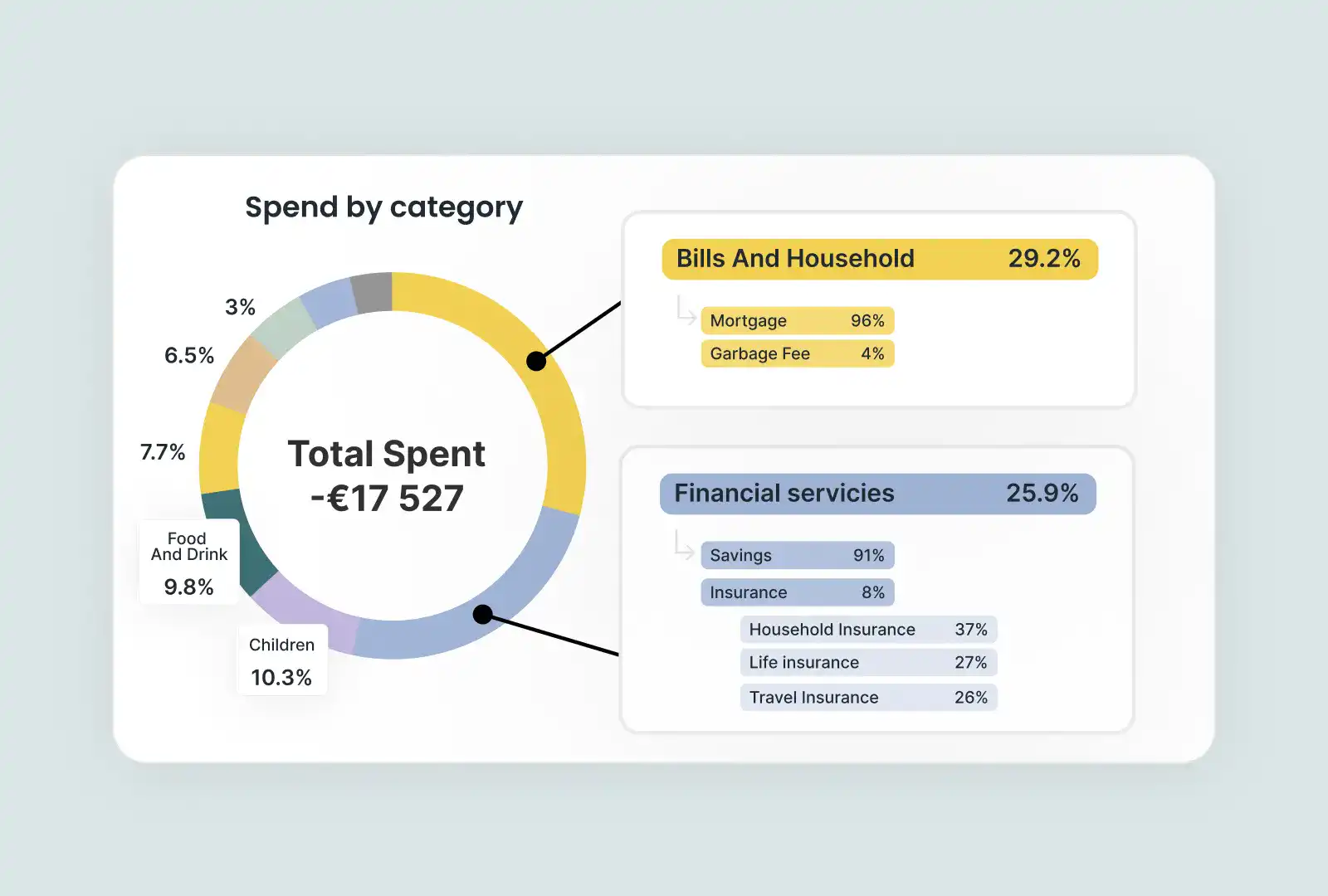

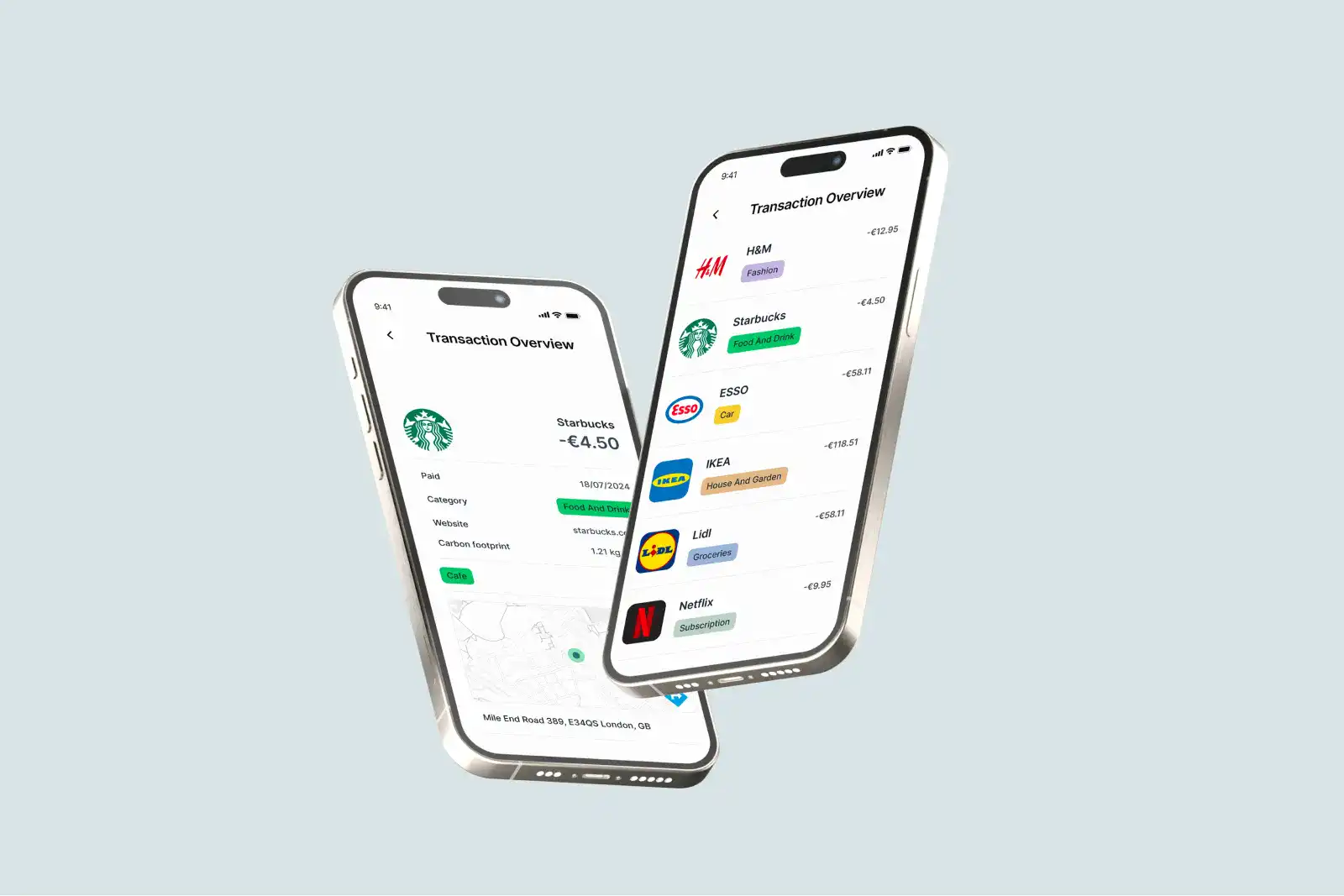

To put simply, transaction data is merchant identity, category (MCC), channel, store hints, amount, frequency, and cadence. Enriched banking feeds now go further: clearer merchant names, recurring-payment detection, even sustainability add-ons; Visa and Mastercard have public examples of the enrichment banks are rolling out across Europe. Cleaner data is the layer that makes spending intelligible to normal humans and reduces charge-confusion.

Let’s look at the steps you can take to level up your retail strategies.

Step 1: Clean the inputs so they’re human

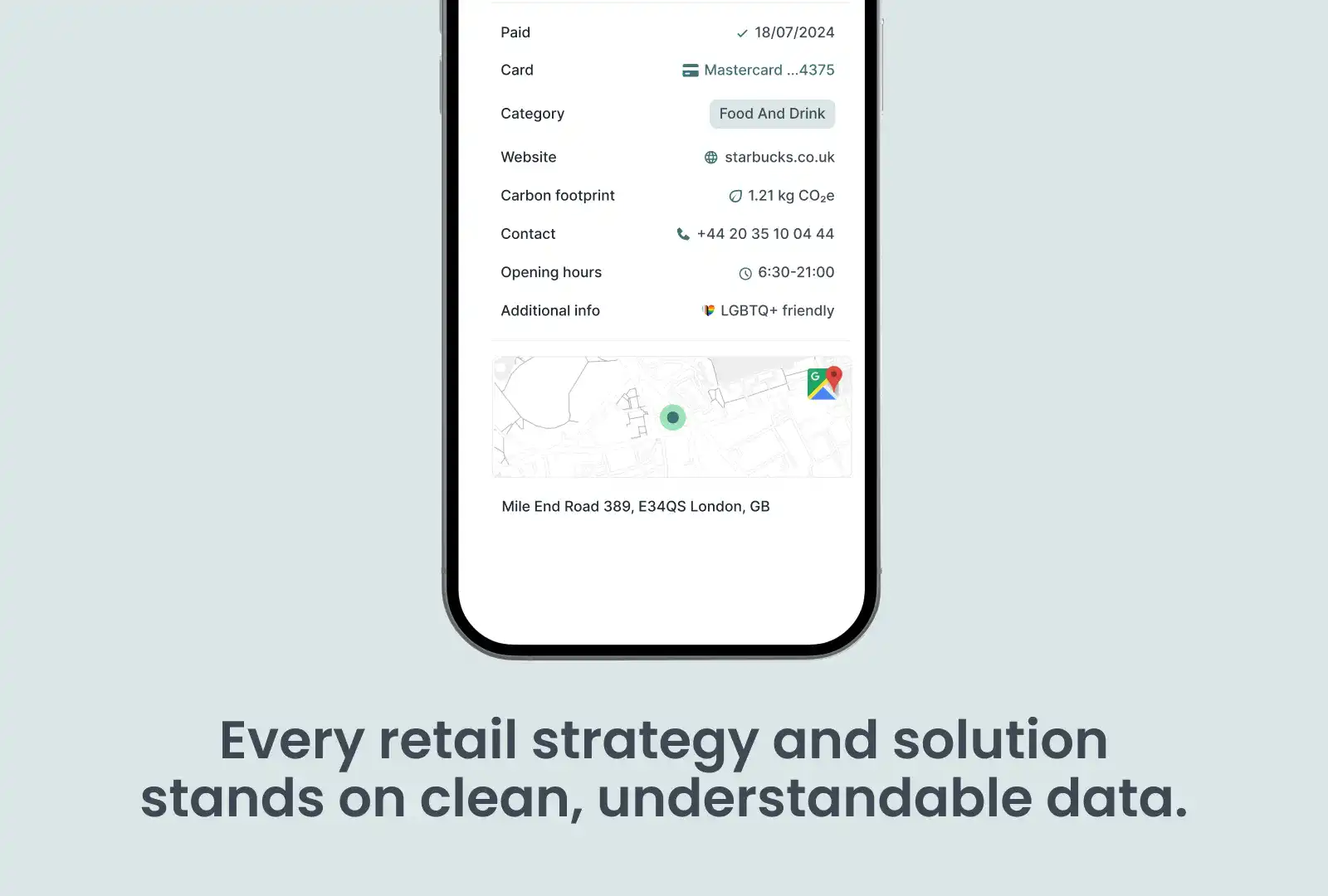

Core data is an obvious baseline before you move forward. Messy descriptors like “AMZN X-10” don’t help a merchant or a customer. Normalise to a canonical brand, attach a logo, map MCCs consistently, and resolve store clusters. This is exactly how big card-linked networks talk about measurement. If merchant resolution is chaotic, everything downstream pays the price.

Do this first step, and you get fewer unknown charge disputes, clearer category spend, and a banking/app experience that customers actually trust. Mastercard’s Consumer Clarity underlines why displaying merchant details cleanly matters at support time.

Step 2: Build segments from spend

Skip segments like “female 25–44” and build audiences from RFM (recency, frequency, monetary value). That means category mix, weekday vs weekend patterns, average ticket, and share-of-wallet vs rivals. You’ll find “grocery weekly, Saturday AM,” “coffee commuter, 4x/month,” “electronics once per quarter.” Those aren’t personas; they’re habits. And habits respond to precise, personalised campaigns.

Why this works? Shoppers, especially younger cardholders, actively hunt rewards that feel easy and relevant. If the offer maps to their spend, they engage. PYMNTS has data showing strong reward-seeking behavior among Gen Z and youngercohorts.

Step 3: Pick the moment, not just the audience

The right buyer at the wrong time still says no. Use cadence. Trigger grocery offers just before the usual shop; show travel insurance after airfare; nudge fuel before long-weekend peaks. This is “routine-level” timing. Publish where attentionalready lives: inside banking apps, on transaction details, or as light push when the pattern repeats. Issuers keep calling out how card-linked placements increase app engagement, which is why these surfaces keep expanding.

It works because third-party cookies are unstable ground for targeting. The policy yo-yo continued through 2025 with multiple reports noting reversals and walk-backs. Purchase data isn’t subject to that drama.

Step 4: Choose the incentive

Cashback changes habits for routine categories; vouchers move bigger, considered baskets. Run them as card-linked offers (CLOs) so activation is one tap and redemption happens automatically on payment. The model is well documented: offerpublished in the bank, user activates, transaction is matched, reward is settled, and lift is measured off actual spend.

Retail playbook examples:

- Acquisition with receipts: target category shoppers who don’t buy your brand; pay only when the tender proves the switch.

- Reactivation with a clock: 60-day lapsed customer gets a time-boxed booster to rebuild the habit.

- Upsell with cadence: device at day 0, accessories at day 7, warranty at day 30.

Step 5: Prove, learn, scale

Run one clear use case. Show lift. Then widen the aperture. A simple pattern works well:

- Start with one category where habit is predictable (grocery, fuel).

- Layer a considered category (fashion, electronics) with vouchers and thresholds.

- Tie post-campaign behavior back to loyalty metrics and lifetime value.

As seasonality hits, feed your plan with category readouts from commerce-media and consulting sources that track spend shifts across billions of transactions and holiday windows. Adjust offers before the rush, not after it.

Bottom line

Transaction data fills the gap because it’s the truth. Clean it, segment by habit, time the moment, pick the right incentive, and measure with receipts. Do that, and retail decisions stop feeling like guesswork and start looking like operations.

FAQs

There are five steps to use transaction data for retail solutions:

- clean the data to make it human-readable,

- build segments based on purchasing habits,

- time offers according to customer routines,

- choose the right incentive, such as cashback or vouchers, and

- prove, learn, and scale campaigns. Following these steps ensures precise personalisation and improved marketing ROI.

A content creator with a passion for emerging tech companies and the startup community. She uses her background in media and PR for writing, editing, and brand building. Her mission is simple: she loves a good story, and strives to make complex topics clear and simple.