Customers don’t want more messages these days. They want fewer, but relevant nudges. When brands get that right, revenue moves. Multiple studies keep repeating the same thing: people expect personalisation and get annoyed when they don’t see it. Companies that do it well grow faster and convert better.

Let’s explore how the retail stack is shifting, and why card-linked offers (CLO) quietly supercharge the whole thing.

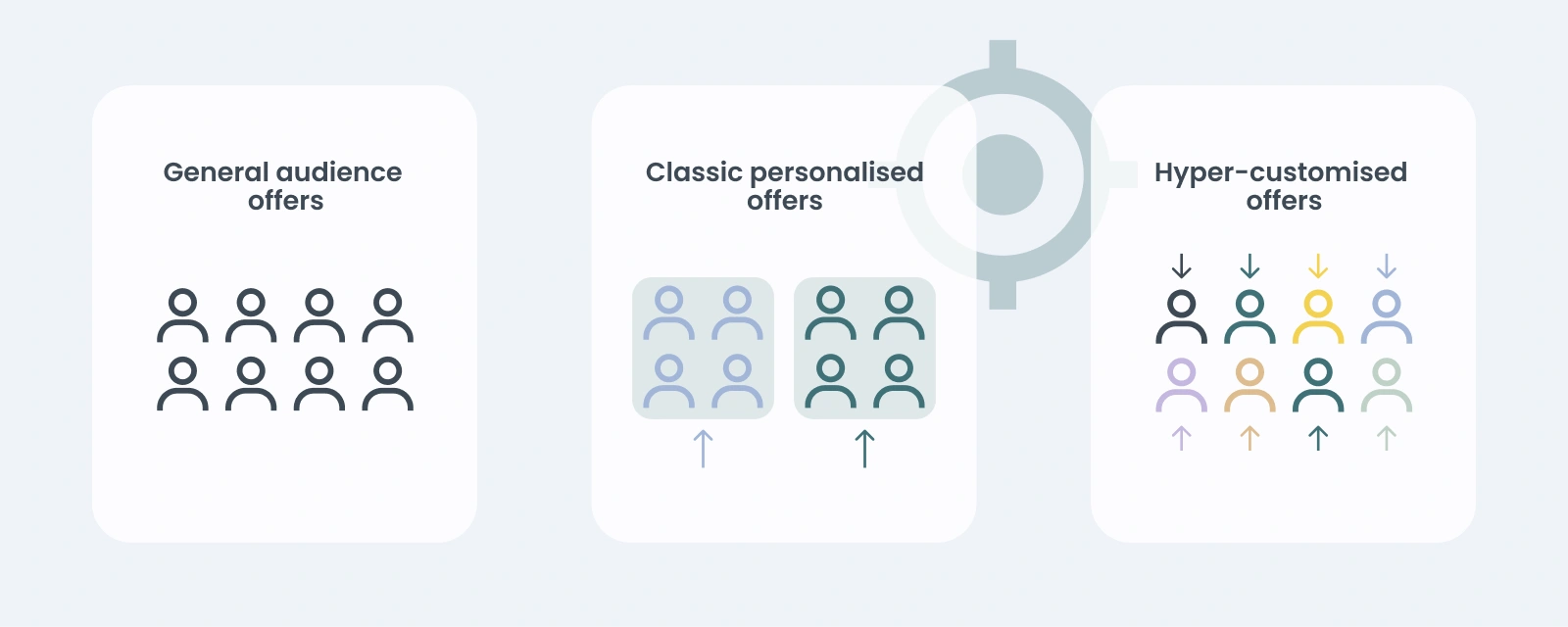

Personalisation vs hyper-personalisation

Personalisation is segment-level relevance. Hyper-personalisation is individual-level timing, context, and content built from real behaviour: what someone buys, how often, where, and with which intent signals. CLO plugs into verified card transactions to trigger rewards automatically and measure outcomes down to each redemption, no cookies involved.

Here are the main points where CLO and hyper-personalisation connect:

1) Consumers expect it, and patience is thin

Most shoppers say they’re comfortable with personalised experiences and they expect brands to deliver them. When brands miss, frustration rises. Consumers now reward relevance with attention - and punish irrelevance by switching brands. The patience threshold has shrunk to seconds and people scroll past generic ads instinctively.

2) It moves hard numbers, not just sentiment

Done properly, personalisation correlates with material revenue lift and lower acquisition costs. You see 5–15% revenue gains on average, with higher ranges for strong executors. Personalisation also drives 5–8x ROI on marketing spend, largely because it reduces wasted impressions and increases relevance. Gartner estimates that failing to personalise can cause brands to lose up to 38% of their customers.

3) Cookies fade, first-party data wins

With signal loss across paid media, retailers need consented, durable data. Transaction and loyalty data become the clean fuel. CLO operates without third-party cookies and ties directly to payment proof, so performance isn’t modeled, it’s recorded since it’s focused on actual transactions.

4) Timing beats volume

A nudge at the right moment outperforms 100 generic emails. Think travel insurance right after a flight purchase or accessories three days after a phone sale. Hyper-personalisation is mostly about timing, and CLO gives you the moment of truth: the payment. The result? Up to 3x higher conversion rates compared to static campaigns.

5) Banking-app distribution lifts engagement

CLOs live inside issuer apps people already check for balances and transactions. That placement boosts discovery, activation, and return visits, especially among younger cohorts who actively seek these offers.

6) It cleans up attribution

Click-based attribution is noisy. Payment-verified outcomes aren’t. CLO shows views, activations, and redemptions tied to incremental spend. That lets marketers compare cashback vs voucher economics without guesswork.

7) Loyalty fatigue needs a better spark

Consumers join lots of programs but engage deeply with only a few. Hyperpersonalised triggers, delivered through CLO or the bank channel, wake up dormant members and make the loyalty layer actually feel rewarding again. For example, a sportswear brand can target active runners, not just registered members, and offer cashback tied to their spend frequency.

8) It’s omnichannel by default

Customers bounce between online and store. CLO tracks the spend either way, applies the benefit automatically, and keeps the experience in one place. No codes, no scanning, no awkward “do you have our app?” at checkout.

9) Privacy can be a feature

Yes, consent rules matter. The Cisco Consumer Privacy Survey found that 86% of consumers care about data privacy and 79% will leave a brand that mishandles their data. Build clear consent flows, purpose descriptions, and easy opt-outs. Retailers that treat privacy as part of UX build trust while staying compliant with GDPR and regional laws.

10) It compounds: better data → better offers → better data

Each relevant interaction trains your system. Purchase patterns refine audiences, improve thresholds, and inform next-best actions across categories. Over time, your program feels less like marketing and more like service.

How CLO makes hyper-personalisation practical

You want precision without friction. CLO checks both boxes.

- Targeting based on verified spend: Reach switchers, loyalists, or lapsed buyers using actual category and merchant history.

- Right reward for the job: Cashback to build frequency; vouchers to push basket size or new categories.

- Live testbed: A/B test reward levels, windows, and audiences; read incrementality off transaction deltas.

- Bank-grade trust: Offers appear where money lives, which reduces skepticism and increases redemption.

CLO isn’t just an issuer toy. For retailers, it’s a performance channel with clear cost-to-sales math and fewer attribution fights.

A simple playbook to get moving

- Pick three journeys where timing matters: new device purchase, weekly grocery run, lapsed fashion buyer.

- Define the job of the reward: frequency vs basket size; acquisition vs reactivation.

- Run two reward types via CLO: cashback for habit-building, voucher for lift.

- Measure incrementality using exposed vs activated groups; track repeat rate for eight weeks.

- Feed learnings into loyalty: adjust tiers, perks, and comms cadence based on observed behaviour.

That’s enough to outpace most competitors who are still arguing about “which channel owns the customer”.

Hyper-personalisation is how retail marketing actually works when the data is clean, the timing is right, and the reward is obvious. CLO adds the missing precision: it targets on real spend, triggers at payment, and measures with receipts. Pair it with a loyalty layer that people want to use, keep privacy honest, and you’ve got a growth engine with fewer leaks.

FAQs

Personalisation targets a customer segment (a broad group). Hyper-personalisation targets a specific individual with precise timing and context, using their real-time behaviour and verified transaction history to deliver maximum relevance.

CLO enables precision by linking directly to verified first-party transaction data, bypassing third-party cookies. This allows targeting based on actual spend and triggers rewards (like cashback) automatically at the point of payment, ensuring the highest level of attribution accuracy across all channels.

Retailers should invest because it drives significant, measurable results: according to McKinsey average revenue gains of 5-15% and high 5-8x ROI. It directly addresses customer demand for relevance, reducing the risk of churn caused by generic messaging and wastage of advertising spend.

Marketing professional with B2B, fintech, e-commerce, and retail experience. She connects banks and retailers through data-driven personalization and commerce media, turning complex topics into engaging stories.